Banking in PH Part II: Raves for BSP transparency & a look at individual banks

This article has three basic parts: (1) praise for BSP transparency, (2) review of Part 1, and (2) scan of individual banks.

This article has three basic parts: (1) praise for BSP transparency, (2) review of Part 1, and (2) scan of individual banks.

Praise for BSP transparency

One of the thing that astounds me is how ignorant I am about what is going on within Philippine government. I draw conclusions easily within this ignorance, and I can see that voters do the same thing. It is surreal how convinced we come to be without knowing anything at all about what government is REALLY doing. Rather, we spend our time concocting elegant defenses of our ignorant position using simplistic or mythical arguments picked up in tabloid media.

It is a huge problem, and . . . granted, we should accept accountability for our lazy presumptuousness . . . but I think it would help if government were to do a better job of popularizing their successes.

Several months ago, I was rummaging around on the web site of the National Economic Development Authority (NEDA) and was impressed with the superior work done to put plans and metrics and data (e.g., status reports on infrastructure investments) into place. These are the stuff of good corporate management. This work is one of the unseen disciplines that President Aquino has put into place (yes, there are disciplines other than Duterte’s “kill them”), and all future administrations will benefit from this fine groundwork. NEDA has continued to develop depth in its plans and reporting, with separate long-term plans being developed for National Development, Manila Transportation and Manila Floods.

When you feel the need to disabuse yourself of the notion that Philippine government is “inept”, visit the NEDA site and prowl around. Presidential candidates should be required to do this. Another site to investigate is the much maligned (for “DAP”) Department of Management and Budget (DBM). Do that and you will join the ranks of the rare, the unique, the informed.

A third data-rich site to visit is Bangko Sentral ng Pilipinas (BSP). Head directly to the Key Statistics page, and click away. Start with metadata. The financial and economic health and wealth of the Philippines is at your fingertips.

I believe President Aquino does not jump and shout for FOI because he knows his agencies have “bought into” transparency, and BSP is leading the way. It helps that the agency MUST HAVE sophisticated computer systems to handle their business, and they can dedicate a portion of that computing power to statistics and reports. That is the track that other agencies are also on, but some have not progressed as far. They will.

Why is FOI needed when the press and even presidential candidates do not trouble to read what is already there?

Kudos to BSP and it’s management team under Secretary of Finance Cesar Purisima Amando M. Tetangco, Jr. World class.

Review of “Banking in the Philippines, Part I, the fundamentals“

In the first section, I wanted to present a basic overview and “sizing” of different elements of the banking industry. We learned that:

- Universal and commercial banks – 40 of them – represent 88.6% of all banking assets.

- There are numerous specialized banks and non-banks, like thrifts, rural and cooperative banks, trust companies and pawnshops (over 17,000 of them!!).

- The assets of the large Universal banks (80% of total assets) are comprised very roughly of 1/4 debt securities, 1/2 well diversified loans (primarily to businesses; consumer loans are minimal), and 1/4 is “other”.

- Funding of assets at Universal banks comes primarily from domestic deposits (85%) collected from branches.

- We structured a “to do list”: (1) look at income and performance ratios of banks, (2) examine individual bank financials, and (3) understand “grass roots” banking better: microfinance, pawn shops and payday loans.

This second installment leads us into individual banks.

A look at individual banks

First, let me provide three excellent reference sources on banking that are derived from the sophisticated regular six-month comprehensive reviews provided by BSP:

- The Philippine Banking System as of June 2015

- The Non-Bank Financial Institutions with Quasi-Banking Functions as of June 2015

- Appendices (Data Tables) as of June 2015

This information is exhaustive, and exhausting to go through. But there are gems in the Banking Report, such as the above chart on banking consolidation. The “Non-Banks” will be looked at in a later blog article, but for those of you interested in this field . . . there you go. The Appendices provide the nitty gritty facts and figures as to how numbers roll up and trend. We’ll dig into a few of them as we proceed.

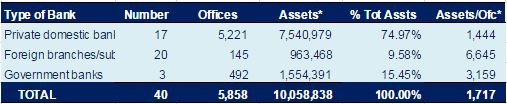

What I learned by searching for individual banks is that there is a better classification than “Universal or Commercial”, and that is to consider banks according to their charter as: (1) Private Banks, (2) Government Banks, or (3) Foreign Branches and Subsidiaries. Here’s how the pie slices:

Local banking is done by private and government banks. Foreign units are mainly centralized in Manila. With new rules for ASEAN integration, we may see more foreign banks with broad networks.

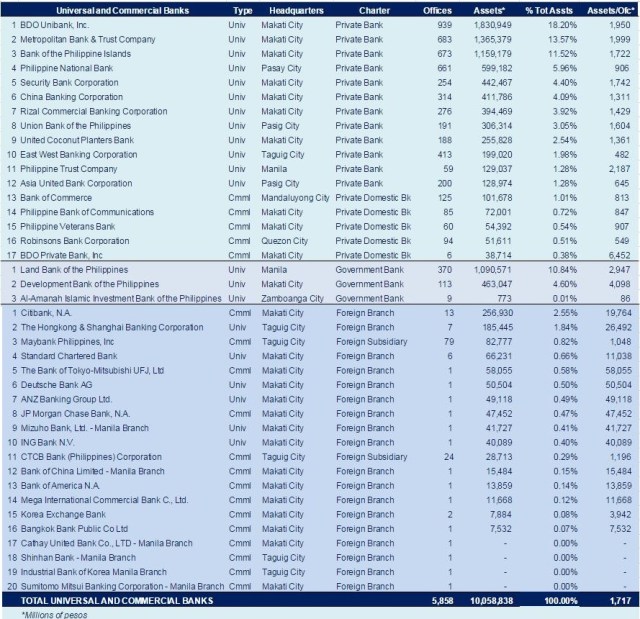

Here’s how the individual banks sort out, ranked by asset size, and reporting number of offices. I apologize for the small type; it’s a lot of information to squeeze in here.

There are four “trillion peso” banks and four “half-trillion peso” banks. In “street lingo”, the four big gorillas, representing 54% of all Universal/Commercial assets, are:

- BDO

- Metrobank

- BPI

- Landbank (Gov’t)

The second tier, representing 19% of all assets, are:

- PNB

- Development Bank (Gov’t)

- Security Bank

- China Bank

As we look at individual banks in detail, I suspect we will find that government bank balance sheets are very different than those of private banks, as the government banks handle CCT payouts and other agency programs.

The next step in digging deeper will be to compare the balance sheets and performance ratios of the four biggest banks.

By way of perspective, at 47 pesos per dollar, BDO, with US$ 39.0 billion in assets, would rank as the 35th largest bank in the United States based on US Federal Reserve rankings.

_______________

Erratum: With apologies, the head of the management team at BSP is Amando M. Tetangco, Jr. as Governor of BSP and Chairman of the Monetary Board.

FOI is a good thing, but people must be able to interpret data correctly and in context – they can’t.

Data is not information is not knowledge is not wisdom. An undergraduate graduates as Bachelor.

Unliquidated Yolanda funds as per COA are NOT stolen money. Davao, Iloilo and Albay prosper.

That’s true. It takes a skilled analyst or specialist to probe the information, and neither journalists nor regular people are inclined to do so. But the law would instill new disciplines, requiring the automation of tasks and reports that are now done manually, and perhaps generate a new breed of social media people who would find the data, and set it up for popular appeal.

If I were Executive in future administrations, I’d continue to have a “data geek” like MLQ3 to probe and popularize the data for journalistic consumption.

http://i.gov.ph/faq/faq-page/pgcp#t11n162 – this is about INTRA-Governmental sharing of data… something DOST has been working on for years… the fiber optics backbone of the government is part of it… Bam Aquino is involved in this BTW… another geek of course. The next step is to share data with the stakeholders, i.e. citizens… but this stuff has to get off the ground first and they are building everything by themselves, not buying abroad.

When you make cash advances and you were not able to produce receipts, then it is like stealing.

As for undergrad, even job recruiters or interviewers,I encountered gets confused with undergrad,when I mentioned undergrad, they asked if I graduated College..

I would say the receipts still have to be produced, so pending that not yet clarified… and what is absurd are the memes circulating that connect Mar Roxas and jump to the conclusion that the money is being used for Fast Forward and other campaign stuff.

My dealings with government people expose me to the general sentiment expressed by Irineo.

The first fear is that the unthinking media just uses this to destroy trust in government because they cannot be bothered to understand or explain things.

The second sentiment against FOI is that save for agencies with sizable IT divisions the burden of producing the information within 2 days to 2 weeks depending on the bill is would create a burden to these agencies.

An example of this is that the DSWD have a separate and relatively well manned team whose job is to update the listahan or list of beneficiaries of its programs.

Sweden has FOI… I think most other Scandinavians and the Dutch have similar stuff to.

Germany does NOT have FOI, nor does it have much direct democracy except for Bavaria. The Swiss have had direct democracy… but in the end you need responsible people for it.

In Bavaria anyone or any group can make a petition… but it has to be signed by a sizable quorum of inhabitants (locally or state-wide depending on scope) with national IDs shown to become a real referendum… and the results of that referendum are binding for 10 yrs.

Example: tall buildings caused some conservatives to start a petition to limit building size to 99 meters, the height of Munich’s cathedral’s. The referendum was a success for them.

But due to the principle of “legal security”, buildings already there were NOT shortened.

On the other hand, it would likely accelerate the application of computer power to make data available in those agencies that today still depend on paper.

*******

A portion of FOI is dedicated to computer infrastructure.

As I opined way before, people do not know the complexity of computer infrastructure required to be set up… to be able to ask for government information a la Google.

*****

In an ideal world, government can share infornation,like BIR can get info from SEC.Or DA can get info from BOC.That can’t even happen yet.

DOST ASTI is working on shared computer base infrastructure for such a system.

What they are finishing as of now is the most vital component – records management.

http://i.gov.ph/narmis/

I like the approach of locally making solutions instead of buying from abroad.

This builds IT skills and a spin-off could be products for sale, eventually.

We may need to take a look on the FOI bill. I think budgeting or at least creating budgeted positions for FOI teams for each agency would go a long way in helping cure the fear that rank and file government employees against FOI.

This reading tells me then that not only are NEDA, BSP and the Banking System doing their job well and have records to show for it, but we in the Philippines have the good fortune that the general political mindset especially the worse half of it has been quarantined in a manner of speaking from these vital institutions. Thank heavens for that.

Ah, a positive outlook for sure.

I am still stunned, though, but how negligent the media are at conveying the truth to citizens, that the Executive branch is doing a WHOLE LOT of things right, and doing them well. It’s unfortunate, and I suppose a shortcoming of the Administration that it has not found a way to popularize its successes.

Hard to show Filipinos work in progress when even the “we will study it” statements of Aquino are seen as “not doing anything”. Charges are now being pressed on “tanim-bala” by NBI, but most people still think nothing was done, ignore the results. How much more for work in progress like IGOV.PH (IT infrastructure both hardware and software for the government) or the DOST AGT (fully locally made train to AVOID MRT problems of having to wait for parts from abroad) – or Lambat-Sibat which was first piloted in Metro Manila, so everybody thinks it didn’t help anything, damn Lambat-Sibat is 100% the Bavarian State Police approach – go for the big fishes using Intel and lightning raids, like FBI stings…

ITEMS

– too many major problems accumulated over time over several administration, traffic congestion in EDSA being one (in this one sadly a lack of simple recognition of vehicle increase, data being there, and road capacity)

– requiring solutions with a non-zero gestation period even with unlimited resources

– limited resources made worse by a long bidding, contracting process because of government procedure and non-aggressive pursuit because of possible corruption charges being made by losing bidders

– layers of red tapes

– non-use of time saving computer tech because it will not allow under the table transactions

– change in admin with the new one with different priority; no continuity

Yes, Irineo a lot of these have been and are being addressed, but we need solutions of all these TODAY. We need a President who can take short-cuts like killing a suspected bad guy as in the movies; no need for court process that takes time. Unfortunately, projects have gestation period and cannot be shortened from years or months to a day — no matter how many heads are made to roll. “Off with his head” just will not do.

And a news reporter like me will likely be fired within weeks if I write out my report considering these nuances. Better for me to report about Presidential Candidate A saying he will slap Candidate B; and that B will slap back A.

it would be easy to suggest Get rid of ten year old vehicles or older.But look at what happened to the squatters relocated to Bulacan and Laguna, they are backto where they came from because besides lack of utilities and services, there is no mass transport.

Off with their heads is like Alice in Wonderland.

Miriam reminds me of the Queen of Hearts.

Nephew, (might be off-topic):

Society blogs have touched on Mamasapano, China incursion, and leadership topics, what is the good/bad news on Lt Gen Cardozo Luna? Just curious on your take. Thanks.

Sorry unc had to google him and read his wikipedia page.

https://en.m.wikipedia.org/wiki/Cardozo_M._Luna

ulk! Heavens, I hope they wouldn’t suggest getting rid of ten year old vehicles, otherwise I will lose my old friend – Isuzu Crosswind XT. It’s still in a fine running condition, well maintained and for family use only. It served us well yesterday, going to Batangas to fetch the old folks, then to Tagaytay City for, then back to Batangas, then home to Metro Manila.

This reminds me of an unhappy and frustrating experience I have with a local bank with regard to that car’s acquisition. We made a substantial DP on it, and the rest was paid by the bank with a 2-year loan. A few months later, we pooled our existing and new funds and came up with an amount enough to pay in full the car loan. I wrote a letter to the bank and requested a computation, expecting a smaller figure since we are planning to fully pay it in advance. Horror of horrors, an answer came telling us that we need to pay the full amount of the loan without the expected interest rebate, in short, we need to pay the computed monthly amortization multiplied by 20 months. After more failed discussions, we decided to just continue with the 20 monthly payments, I didn’t have the energy to be my normal argumentative self as my mother’s health has worsened and doctors are already asking us to sign a DNR (Do Not Resuscitate) and she died not long after that.

I lost the will to report the bank to the BSP.

Car loans she structured that way Mary. It is a fixed percent fixed term loan. I asked the loan officer why it is structured that way and she answered that the loan would not be worth the risk if it is structured like a housing loan.

Yep, you might be right there, Gian. That’s what the bank officers told me in one of their responses to my pangungulit. Although it could depend on the banks giving the car loan. My brother-in-law was given a proportionate rebate when it was his turn to make an advance full payment. He did it with BDO and East West Bank for two his cars, bless them.

This is a good point since we are talking of banking environment in Philippines. Perhaps Joe should take this up. I think what’s missing here is hire-purchase financing. I don’t think there is such an act in Philippines. Car financing, as well as big item equipment financing, is mostly done this way in other countries. Under hire-purchase, the accounting is also done differently.

The problem is therefore the readership… the market drives the need.

Data is not information is not knowledge, much less wisdom.

Most of the stuff in the papers is data… Inquirer, PDI etc.

Rappler, Interaksyon and CNN Philippines at least offer information.

Mindanews actually offers some knowledge, but mostly about Mindanao.

In fact I have seen some Mindanews editorials which are wise, very wise…

PiE, deja vu, viz data pathways & data access-transfers speeds, thruput to I/O devices: CPU, cache (nanosecs), DASD devices (microsecs), I/O (display, print, microfiche, CDs etc), etc … and of course, telephone lines. These basic data processings concepts MUST become the classroom stuff for young and old alike. This level does not necessarily need individual hardware, a well-designed combination of demo and queued hands-on will do the job like basic English, arithmetic, algebra. We must transition from data-users to information users if we must skip information chauvinism at all levels, obfuscation at the media level and demagoguery at the governance level. I think.

back to bsp transparency. Since I accidentally posted this in another blogpost might as well repost it here.RHiro,being a forensic financial analyst,often has something to say with BSP data.So he will be one to disagree with the citing of BSP’s transparency.

I tried to log in at 7:06 am today Dec. 16, 2015, Wednesday, to post on your article about critical thinking vs thinking critically, but could not get connected; so I guess I have been banned without notice but by just being locked out.

Or perhaps some connection problem from the part of your transmission station?

Please inform.

Maybe its just the inclement weather.But, your comment post worked here,what about commenting on other topics like most of us?

If you insist on that topic,I saw a request to talk about Jesus by Lance Corporal X.

The site has not been down and you are not blocked.

I’ve been a lurker here since Joe was yet the only blogger. I must now “out” myself because of this part of the blog:

“Kudos to BSP and it’s management team under Secretary of Finance Cesar Purisima. World class.”

I was with BSP for 31 years and kind of proud for that.

But please let it be known that Mr. Purisima is only a member of the Monetary Board as government representative. The guy that is head of the management team is Amando M. Tetangco, Jr. as Governor of BSP and Chairman of the Monetary Board.

I was about to share this with friends at BSP but I have to wait until the erratum is acknowledged.

Rank Merida

Just a little edit on paragraph 3.

I was with BSP for 31 years and this blog makes me, kind of, proud for that.

Thanks for the correction, Rank. I for sure regret the error, and I’ve changed the report accordingly.

@ Rank

I was going to raise this point too, you may have noted I gave credit to Tetangco in my previous articles.

But I’m glad too that you bothered to come forth on this, as you rightly should.

i look at the banking system a necessary evil. on one hand it is somewhat a ponzi scam and on the other hand it facilitates trade and exchange. ponzi scam because what the depositor puts in is not what it gets out, though it may seem that it is arithmetically at least equal or more, but in real value it is not. the banker (owner) is all the time the winner because he gets paid for the services. when the

banking institution goes kaput, the losers are always the depositors and the institution itself. because of inside information in the banking system, the owners can always remove their investment so that they are able to take out what they put in. and what is left in the institution’s coffer, this and the insurer’s guarantee will be returned to the depositors…and most of the time, the amount returned is less than what is the depositor’s account balance.

the banking institution becomes tenable if money is always going in to the institution so it can pay the interest of the depositor and any withdrawals. what if each depositor will take out all their deposit? the assets of a bank seem to grow big arithmetically due to inflation and accounting magic but its real value does not.

in the bank we deposit money. if one deposit $100 at an interest of 2%pa, one would be able to get $102 after a year. the bank will then loan this at 6%pa to a borrower. thus the bank makes a clear take of 5% by being the go between the depositor and the borrower. if we deposited 100 grams of gold, by same logic the bank will get 5grams of gold. if it lends the 100grams of gold, the bank makes money.

but when one deposits 100 grams of gold to the bank, they will credit the value of the gold at the time one has deposited it. for simple calculation, let us say the price of gold is $100 per gram. if mr a deposited 100 grams of gold on 1 jan 2016, mr a is credited $10,000 (and mr a agrees that this is his gold money now). and on 1jan 2017, mr a will have $10,100 not 100 grams of gold. on 1may 2016, the price of gold went up by $4 per gram so the bank gold money became $10,400. the bank clearly made $200 (the other $200 is to pay the interest). and if he loaned this gold money, the bank will have earned another $600. wow that is a good $800 just being the go between…mr a gives money to mr bank and mr bank loans to mr c.

unless a good deposit contract is made, the reality is mr. a sold the 100grams of gold to the bank and the proceeds of the sale is credited to mr. a’s bank account. if mr a thinks he lost in the transaction then he needs a good lawyer to get back his gold.

as a simple man, in a nutshell this i think is how banks operates, they provide service and they should be compensated for the service. where i disagree with some of the banks operations is the bank owners get their lavish lifestyle on the back of the ordinary depositor. i just made the numbers small so it is easy to do the aritmethic. think of the gold as the collateral for the exchange/loan and the loan interest is not really 6% but much higher.

Nice analysis, wangad. Yes, a deposit that earns 1% when inflation is 3% is actually a negative-earning investment. The problem is, there are few places that we can invest money that is risk free and safer than home in the closet . . . so a bank provides us that service. On the lending side, the bank takes a lot of risk, and that is the highest value of a bank, and why they deserve to make a healthy profit. When they loan $100 and the loan goes bad, they don’t lose the interest amount of, say 9%, they lose the whole $100. So they have to make 11 more good loans at 9% to recapture for the loss (setting expenses aside).

Banks provide a valuable function, reasonable security for deposits and reasonably priced loans. I have not gotten to the regulatory aspect yet. In the US, they are closely regulated, so failures are rare and are “covered” by regulators, and banks are well-run businesses for the most part.

“When they loan $100 and the loan goes bad, they don’t lose the interest amount of, say 9%, they lose the whole $100. So they have to make 11 more good loans at 9% to recapture for the loss (setting expenses aside).”

That’s not exactly true Joe. When loans go bad, banks would confiscate either your collateral or the asset that you built/purchased using that loan money. In the case of home mortgages going bad for example, banks would kick you out and re-possess the house.

The real estate developer gets fully paid, the borrower lost the house and is now living in the streets, and the bank is in possession of a real asset which it could re-sell to another loan applicant.

Bank of America alone is in possession of hundreds of thousands of these home mortgages gone bad and is set to make a handsome profit as the real estate market recovers.

Micha your comment is obviously correct in respect of the banks course of action as regards the borrowers directly. I think Joe is making the point that in the banking business the loan pricing takes into consideration the need to cover delinquencies. This is factored into the margins and thus rate spreads are high, thus Wangad’s gripe that he earns 2% whilst bank’s earns 6% at his expense. And that is the reason why credit card interest rates are exhorbitantly high, especially in Philippines, because card delinquencies here are way too high.

Right.

@chempo

I’m not taking issue with the discrepancy between deposit rate and the lending rate. Indeed that’s how the bank’s racket or usury is done.

I’m taking issue with the claim that when the borrower defaults, the bank losses “the whole $100”. In most if not all circumstances, borrowers default after they already have settled part of the loan by paying the monthly dues.

That’s in addition to the fact that if a borrower do indeed eventually defaults, the banks could resort to either confiscating the borrower’s collateral and/or assets.

I understand your point but you are still not getting my point.

Right now, I’m not interested in how banks price their loans. That’s just profiteering, pure and simple.

Usury is generally defined to mean illegally high interest rates, and banks do not charge usurious rates. Even pawn shops here are regulated and charge rates allowed by law. Now, I consider banking not to be a “racket” but a legitimate intermediary function. Whether pawn shops fit that description yet, I don’t know. It’s a topic for further investigation and discussion.

usury is still illegal in the Philippines but the Central Bank don’t set maximum rates anymore so the law becomes ineffective

That would certainly gut the law.

In other countries where banking is competitive, Micha’s charge of profiteering is outrageously so untrue. Banks try to outbid each other to tenths of basis points for heaven’s sake.

I have an office mate who made the mistake of paying only the minimum amount due as billed by the credit card company. Her world came tumbling down when she eventually realized that her 20K credit limit ballooned into more than 400K in outstanding bills as she taught she could continue her shopping sprees (for her family needs). Lawyers came to the office and attempted a garnishment proceedings against her salary. It took her 48 PDCs to fully settle her obligation (extra judicially) and vowed never to touch another credit card again.

Am so fond of using that plastic money myself, but am so stingy when it comes to unnecessary interest payments, the credit card company does not earn a single centavo from me, I’m told that they get their income from the business merchants, as I settle in full every month, even my annual fee is waived for life. The best is Union Bank, which gave me a 100K non interest loan just by agreeing to activate my credit card with them, which I haven’t done so for years.

Why are banks sharing their client’s confidential information with each other? I asked them when I receive so many unsolicited, pre-approved credit cards from numerous banks as they know most of my personal info, but I couldn’t get a straight answer only evasive ones.

I wonder if this is legal.

Good for you Mary. Discipline is needed if you want to use credit cards.

Many credit card holders make these mistakes:

– They use the card for big item purchases. That is a No-No. Credit card is not a financing facility. It’s a convenience and security facility.

– They don’t understand the rates are extremely high, which means you need to pay off immediately. They moment you stretch payments, your woes begin.

– They don’y understand that for the privilege of using the cards, they need to help the bank to defray their high delinquency costs.

As regards selling confidential info, I can vouch for that. There was a time I was using Amex card member listings for a business project. I got from a friend of a friend.

I don’t know if it is legal or not. The credit rating agencies in the US provide a valuable service by sharing credit histories. It is one of the elements that keeps rates down. The problem in the Philippines is that there are people who could benefit from borrowing because they have a steady job and can acquire a car or home on the expectation of continued good earning power IF they can establish a track record. It’s hard to establish that track record, therefore banks play their games to make sure they come out whole. I will do a blog, I think, to research what agencies do exist, whether laws permit sharing of information, and figure out if this is an area where growth is being blocked by poor information systems.

Back when I was still in that financial intermediary, I remember that the company was a member of CMAP – Credit Management Association of the Philippines.

But the info shared is the credit worthiness of respective clients when requested and when available, not personal and confidential information.

There should be rules to identify what can be shared and what cannot. I’ve not studied that.

I don’t know if it is legal or not. The credit rating agencies in the US provide a valuable service by sharing credit histories. It is one of the elements that keeps rates down. The problem in the Philippines is that there are people who could benefit from borrowing because they have a steady job and can acquire a car or home on the expectation of continued good earning power IF they can establish a track record. It’s hard to establish that track record, therefore banks play their games to make sure they come out whole. I will do a blog, I think, to research what agencies do exist, whether laws permit sharing of information, and figure out if this is an area where growth is being blocked by poor information systems.

That is what we need,credit rating agencies.

The top Five credit card companies partnered with TransUnion.

http://business.inquirer.net/11703/5-banks-set-up-credit-bureau-to-keep-track-of-good-bad-borrowers

Thanks. I appreciate the resource. I note that was 2011, so it should be cookin’ by now. The potential is to identify good borrowers and reduce rates to them.

The interest to the depositor is not the only cost of the bank. they could not loan this deposit 100% too because of reserve requirement. they also insure these deposits. and of course theres overhead.

some banks here in the US don’t want even deposits because they have nowhere to park or lend. so its a cost for them. so instead of giving you miniscule interest, they charge you for safekeeping. (that’s the cost to insure the deposit + Overhead)

it is understable that the BSP and the NEDA have good data bases or research. the industry is populated by competent people. it is also meritorious. a clerk in a bank can expect to climb the ranks of a bank.

I even know a security guard of bank who became a lawyer and later on a VP.

for NEDA, they get “all” the scholarships awards to study abroad. so the expectations is high and they deliver. the problem is the politicians don’t want to use whatever they recommend.

Excellent points, DAgimas. It’s good to know that there are career paths in banking. I agree NEDA is under-appreciated, not just by politicians, but the people in general. There IS professionalism within the Philippines. We are led to believe otherwise by a few agencies that jerk us around (LTO, Customs).

if you come from an unknown school (not a cum laude from the big 3), you start as clerk..its a great equalizer really..after 5 years rotating from various low level positions, you must have learned how to play office politics already then you start climbing the ranks (joke with some truth to it)

generally, banking (for the bankers) is about sales..how much deposits you generate, how much loans you lent..thats how they measure your competence (more or less). the higher your sales, the faster you climb the ranks

That is the same as in the US, including the office politics. Branches here are STARTING to get into the customer-service, sales mode, but they mainly aim it at the people with large deposits. Land Bank is not on that course, though, it would seem. Still authoritarian.

it helps too that the BSP pays its employees higher than an ordinary government agency

Ahhh, another good point.

For updated understanding of modern banking :

http://positivemoney.org/how-money-works/proof-that-banks-create-money/

Extract:

“In the modern economy, most money takes the form of bank deposits. But how those bank deposits are created is often misunderstood: the principal way is through commercial banks making loans. Whenever a bank makes a loan, it simultaneously creates a matching deposit in the borrower’s bank account, thereby creating new money.”

“Commercial banks create money, in the form of bank deposits, by making new loans. When a bank makes a loan, for example to someone taking out a mortgage to buy a house, it does not typically do so by giving them thousands of pounds worth of banknotes. Instead, it credits their bank account with a bank deposit of the size of the mortgage. At that moment, new money is created. For this reason, some economists have referred to bank deposits as ‘fountain pen money’, created at the stroke of bankers’ pens when they approve loans.”

*******

Does not the money that the bank lends come from somewhere? Meaning the money pre-exists?

*****

Nope, new money is created ex nihilo when banks approve a loan.

*******

Thanks. My layman’s understanding is that the loan comes from the deposits of other bank accounts that are merged to form a pool.

*****

That’s the old or classical form of understanding shared by both Joe and chempo.

This is an official paper coming from no less than the Bank of England explaining how modern banking and money creation is done :

http://www.bankofengland.co.uk/publications/Documents/quarterlybulletin/2014/qb14q1prereleasemoneyintro.pdf#page=4

MIcha, we are going round in circles in this discussion. Go back to my old article on bank credit expansion.

Let me re-state and clarify here:

Let’s use the First Cause scenario. Start from Day-0, where Bank L has no money at all.

Day 1- Bank L gives you a 10,000 loan – a simple way works like this (there are a few ways):

It creates a loan account and debit this a/c 10,000

You open a current a/c and the bank credits this a/c 10,000.

So Viola, per Micha’ penstroke

What happens here? 10,000 electronic money is created because you have money in your a/c. Money supply is increased by 10,000 because deposit money goes up.

The Bank L does not need to wait for any money from depositors money to come in before they create the loan. WHY? Because there is no funds moving YET. Nothing has moved.

Now comes the close of business. The Bank L needs to find 2,000 to deposit into their Bangko Sentral reserve a/c. Where to get this money if during the course of the day they have not received some money from other depositors? Of course the bank may borrow overnight in the money market – this is one option which let’s say they borrow from Bangko Sentral.

Bangko Sentral will:

Credit Bank L reserve a/c 2,000

Debit ??? (Let’s say Cash a/c) – 2,000

So Viola, per Micha’s penstroke

Day 2- you decided to drawdown on your current a/c (what’s the loan for anyway if not to be used?). So you write a 10,000 cash cheque and go to the bank. Now how is the bank going to pay you? Where is the cash coming from? You got no funds at all???

To make it more complicated, instead of cash cheque, you write a payee cheque your landlord who banks in into his a/c at BDO. Still no problem for Bank L because there is no funds movement.

Day 3 – the check clears. What does this mean? It means Bank L tells the Clearing House the 10,000 check drawn on them (Bank L) is good for payment. So Clearing House clears the transaction for Bangko Sentral to effect the settlement.

Now comes the close of business. Bangko Sentral will move funds from Bank L to DBO’s reserve a/c.

Credit BDO reserve a/c 10,000

Debit Bank L reserve a/c 10,000

So Viola, per Micha’s penstroke. NOT SO FAST. Can you tell me how much funds is there in this a/c? Only 2,000. Bank L is out of funds by 8,000. Where is this money coming from?

If Edgar is perplexed, so am I. Where is the money coming from?

From theorists’ fancifully worded treatise, money is not needed. The problem only comes when we actually ask “Where is the money?”

Jesus, we’ve already covered this. But because it’s Christmas, I’d supply the tutoring for free for the nth time :

Thanks for the gift haha.

Micha you and I understand the material because our English is alright (RHiro might not agree to this haha). Our disconnect is that we interpret the real world part differently. An academic description of a system necessitates envisioning it a model, that I appreciate. You still place the model in the air, whilst I place the model on the ground.

Let’s just ask practical questions. In my illustration above, just tell me where is the money of Bank L coming from to pay out the 10,000 loans?

chempo, do you understand what ex nihilo means?

The bank creates new money out of nothing by giving out loans.

How much more simpler an explanation do you need?

Ex nihilo.

Out of nothing.

Capisce?

Micha

Creating out of nothing is one point of view, which I understand. As in imy illustration above, Bank L simply debit a loan a/c and give the money to borrower by crediting his current a/c. YES that much is creating out of nothing. BUT then, how is the bank going to give the borrower when he wants it — in CASH? Even if it’s in payee check, sure the net operation will be central bank debit and credit the borrower’s bank (the drawee bank) and the bank who receives the borrower’s check. But where is the drawee bank going to get the money to put in their a/c with the central bank in the first place?

Micha you simply cannot see the operational part, you only view models and interpret it in theoretical dimension.

Just bear me out in this, cos you say Joe and I only hold a classical view — in relation to bank credit expansion.

Now I have described it in detail before, so I’ll just shorten it. In systems with reserve ratios, such as Phils, it’s as described in traditional textbooks. Say the ratio is 10%, so a depo of 1,000 a bank lends out 1,000-100, next bank lends out 900-90,and so on. Total creation of money is 10x. Now that’s a mathematical model. And you were thinking we classical types think that the bank will wait for a deposit of 1,000 and then approve a loan of 900, and next bank waits for depo of 900 then loans out 810. GOD you must be so niaeve to think that. It’s just a model that explains the big picture of what happens in credit expansion.

Actual bank lending has nothing to do with this model. Lending activity goes on independently of the deposit side of the bank’s daily business. The Loan Manager can make all the loans that he want, but he better be good pals with his Treasury Manager who has to look for the money to fund all those loans.

Certain parts of the whole process are yes, keystrokes. But there are real money for goodness sake.

I defer to you to continue this conversation, chempo. We are echoing each other, but Mica is not hearing.

Edgar, banks are required to have a balance sheet with assets (cash, loans, property) and liabilities (deposits, borrowed money) plus equity, like any business. They pool their funding to make loans, so generally, yes, there are deposits backing the loans. They don’t just have assets (loans) backed by nothing. I think Micha is making one of his theoretical points that, in application, mystifies me.

Joe read the link. And give yourself a gift of understanding modern banking.

Modern banking is the same old banking. You take deposits and you lend them out and make money. It is stored and transferred in electronic form. That esoteric, theoretical stuff is good for the academicians who have never run a bank and argue irrelevancies. Relevant is when a customer takes bank notes and entrusts them to the bank for safekeeping and whatever interest is available, and when a customer wants a loan to buy a car, and get’s a manager’s check to the auto dealer. The bank facilitates those needs, and is not the bogeyman, profiteer you make it out to be.

Now the auto dealer takes the check, deposits it to his account, and somewhere in Tokyo, it is withdrawn to build another Lexus, and a part goes to profits (and dividends), and that’s how the real world works.

Evidently, you didn’t bother to read the link at all. Sad.

I read parts of it, and it says what I was saying, why people deposit money (security). But when it moves into the economic stratosphere to describe the making of deposits through lending, well, that is a break into academics away from the business of banking. A bank raises deposits and lends them out. The matter of money circulation is pertinent to the Fed, perhaps, but not to bankers at work, attending the ALMC meetings to get their maturities matched and going to Credit Committee meetings to get the loan quality right. Don’t be sad. Go get a job at a bank and meet the real world.

How much more real can a Bank of England press release on money creation get?

It’s not in the stratosphere, it’s anchored on solid ground.

It’s not too late for you to learn the trade.

97% of money in circulation are bank created money.

Wrap your head around it.

The Bank of England is a central bank, like the Fed. They are concerned about things that bankers who generate deposits and make loans are not. I recall as a young executive working on a paper for my boss that I made reference to money circulation and he threw the paper back at me. “Get that out of there. It is nonsense.”

What we have, as chempo has noted, is two different perspectives. One, economic. That’s yours. The other, business. That’s mine. The economic perspective is valuable for those who set monetary policy and rates, and is not something everyday bankers need to get distracted about. I know the trade, having worked in it for 30 years. I did not work in academia or at the Fed. They have a different job. Different information. Different disciplines. Wrap your head around that.

Uh ok, so you were just a poor banker trying to corner as much deposits as you can so you could lend it out to somebody else?

Why is it that you and R. Hiro take on this snide attitude of intellectual superiority and condescension? Is that taught in college economics programs or what?

You gave me a reading assignment, and I offer one to you. Banking schools often make use of a banking simulation course built on a a model which takes decisions the managers make and translate them into results for the bank. This link profiles that simulation and will give you an idea of the disciplines that are taught. They are very pragmatic disciplines. You only need read the first page and a half; the rest is optional.

https://journals.tdl.org/absel/index.php/absel/article/viewFile/2584/2533

Basically, yes, in answer to your question. That is exactly what I did, generate deposits, although I was not a “poor” banker, but a business executive. And, yes, our job was also to generate as many high quality loans as we could to both the consumer and business sectors. It was and is an honorable profession.

Further, what the Bank of England paper describes is the nature of modern banking itself. There is no economic or business distinction, just operational description.

If you don’t mind Joe, when did you retire as a banker? The reason I ask is that the BOE paper came out only in 2014.

That may offer a clue to the discrepancy in our perspective.

I retired a number of years ago, but the difference in perspective has to do with the usefulness of the information. Bankers are not economists, they are businessmen creating and selling product and operating under rules aimed at keeping depositor funds safe. A central bank has a different job, and the insights you present I presume has more value to them. To convince me otherwise, you would have to show an example of how a commercial bank changed its operating routines based on the new way of looking at things.

@ Joe

BOE, and some other countries, do not use Reserve Ratios and what this means is that banks capability for credit expansion is infinity. BOE prefers to regulate liquidity by using what they call Liquidity ratios, which basically means a bank’s deposit base must have certain % of specified liquid assets. To this extent, BOE, as compared to Banbgko Sentral, has a tougher job managing money supply. This is nothing revolutionary. Been going on for ages in some countries.

When you simplify everything, the business of banking is twofold — attract depositors like hell and lend out judiciously. Has never changed even with the advent of computers. Micha cannot see deposit and loan being independent operational processes.

Interesting on BOE. I didn’t know that. I’m for sure not an expert on central bank ideology and practice, but I know domestic banking as done in the US.

*******

Monetary theory seems to be more convoluted and arcane than theology.

*****

At least the religions have a reference book. The economic priests all print their own.

@chempo

My sister-in-law also works as a personal banker at Bank of America branch. Her job, according to her, is to collect deposits. I asked her one day how does her bank process loan applications and she said she has very little idea because loans are handled by different bank department.

So yes, I understand perfectly that deposits and loans are processed independently.

And right there is your clue that deposits don’t create loans.

It is an intellectual concept that has no applied value as far as I can tell. Rather like seeing clouds as animals does not make real animals.

@ Micha

So please to ask your sister-in-law for what is the purpose of her collecting all those deposit money from her private banking clients?

Now I’m not sure how private banking is done in her bank. In international banks private banking is not a simple case of attracting deposits. They are managing their clients portfolio. Meaning clients put money with the bank and they invest for them in whatever products they can sell them, be it equities, foreign-exchange, options trading, mortgage securities, etc. In other words, it’s not deposit money.

But I suspect in Phiilippines, because banking is not yet that sophisticated, getting customers to place in time deposits are also called private banking. If that is the case, ask your sister-in-law where all those funds go and are they real money?

Geez chempo, depositors open bank accounts to facilitate ease of transactions like paying utility bills. SSS pensioners open bank accounts so that their monthly gov’t checks gets directly deposited. Ditto with students who are grantees of scholarships. Or employees receiving monthly salaries. Bank fees of varying amounts are charged in each of those transactions. Banks make money on those services. That’s the purpose for brick and mortar banks.

Investment banking, on the other hand, is handled entirely by different bank department. That dual ability of banks – the traditional brick and mortar and investment banking – was enabled when the Glass-Steagall Act was abolished and allowed most major banks to engage in excessive risk taking which precipitated the financial crisis of 2008.

Yes. It’s the Egyptian’s concept of grain loans and Dojima Rice Exchange in 1697. The ideas are still useful today.

Micha: “Nope, new money is created ex nihilo when banks approve a loan.”

Edgar Lores: “Does not the money that the bank lends come from somewhere? Meaning the money pre-exists?”

As far as I know nothing has been created ex nihilo since the big bang. Banks cannot lend unless they first have the money to lend.

Chempo: “Let’s use the First Cause scenario. Start from Day-0, where Bank L has no money at all.”

A bank, just like any corporation, is required to have the necessary capital before it is allowed to operate. This can be a source of the money for the loans.

Can a bank operate and earn money without depositors? Technically, yes. It can earn from its borrowers or from its investments in stocks. But it can earn more by borrowing from the public at, say, 1% interest and lending it to others at 6%. (I think that is not profiteering.) The people from whom the bank borrows are its depositors. And the money it borrowed are called deposits. Deposits, particularly, demand deposits are part of the money supply that is termed M1.

Now this is where fractional reserve banking comes in. For our discussion, the main purpose is to serve the depositors. (The reserve requirement is also used in tweaking the money supply). If all deposits are lent out, there will be no need for those ATMs and withdrawal slips since there is nothing to withdraw. So a bank maintains a fraction of its deposit in ready cash in its vault and ATMs to serve withdrawals. But much of its reserve is maintained with the central bank.

When does the creation of money happen? If Pedro borrows P1,000 from PNB and he has a deposit at PNB, the P1000 is credited to his deposit. So the total deposits in the books of PNB is now plus P1,000. Or suppose Pedro has a deposit account instead with DBP and he deposits his PNB check of P1000 to his DBP account, the deposits of DBP has now increased by P1,000. Now remember that deposit is money so the bank has just created money with the deposit of Pedro.

Whether PNB or DBP, fractional reserve requirement steps in. The bank with the additional deposit must now maintain a reserve for the P1,000. If the reserve requirement is 10% then the bank will only have P900 to relend to another borrower and so on and so forth. According to a book by Paul Samuelson this process of deposit or money creation will come to an end when the total deposits have reached P10,000. And granting that there is no leakage in the process.

The BSP reserve requirement for deposits is 20% as of May 2014.

As for that BOE link provided by Micha this is what it says:

When a bank makes a loan to one of its customers it simply credits the customer’s account with a higher deposit balance. At that instant, new money is created.

The additional deposit was created from the loan that was approved. The bank had money to loan.

Suppose Bank of London has just opened. And BOE allowed it to open without any money anyway it can create money from loans it will grant. Here comes Pedro, its very first customer, applying for a loan. As requirement for the loan, Pedro opened an account with the bank. His loan was approved in the amount of 1000 pound and credited to his deposit. Voila, (as Chempo would say) the bank has created money ex nihilo (as Micha would say). Suppose that Pedro will withdraw his money in cash, will the Bank of London be able to serve the withdrawal?

Thank you Rank.

A bank’s loan-to-deposit ratio is one of the common metrics for assessing a bank’s performance.

you can not loan what you don’t have. a $1.00 deposit can only be lent up to what the Central Bank says you can lend. say for example the reserve deposit is 20% according to Central Bank, the bank can only lend $0.80 of the $1.00 deposit. the $0.20 must be deposited to the Central Bank. that’s how it works. even the capital of the bank can not be lent 100%.

these deposit levels are monitored daily because it says how much the bank can lend for the day.

again, you can not lend if you don’t have deposits. and these deposits have costs. you have to insure them and you have to pay interest

Had an uncle (an unreachable richie rich part of the clan) who’s now retired. He worked as a BSP director. It’s only now that I came to think about it, I could have approached him and asked for his help so I can apply there right after the financing firm (engaged in a quasi banking functions) was dissolved by the stockholders. Now, why didn’t I ever think of that? Serves me right for not visiting the province more frequently in those days.

Working at BSP is for sure the cream of the crop employment even to this day, that is, except being a plundering politician.

With the recent spate of ATM card skimming scams reported in the media, I transferred my payroll ATM savings account from a local bank to Land Bank savings account with a passbook. Got a scare when I think of how I deny myself the worldly pleasures of eating (Eating for pleasure easier to overdo than eating when hungry – Heidi Godman) and traveling abroad only to be a victim of sophisticated thieves. I was pleasantly surprised to find out that Land Bank offers high interest rates for individual savers comparative to corporate investors.

Try it. Any interest rate higher than less than 1% is way better.

banks in the Philippines are just prima donnas. when I was working in the bank, any shortage is shouldered by the employee concerned. I mean, its the fault of the employee but they should give allowance also.

same thing with these scams. unless they can prove that it is the depositors fault, they should credit immediately the missing funds.

compared that to the US, when an unauthorized withdrawal is made and you reported it, they immediately credit your account. you don’t have to visit the bank and give statement. a call or email is enough.

Banking fundamentals here seem to be about 30 years behind modern bank operating standards when it comes to customer service.

http://tankler.com/only-phl-banks-got-positive-outlook-for-2016-in-asia-pacific-fitch-3956

For 2016, Philippines is the only banking market in the Asia Pacific region that has registered a positive outlook, according to Fitch Ratings.

“Philippine banks’ generally-high capitalization, healthy funding and liquidity, and satisfactory loan-loss reserves help to balance the risks from relatively high credit growth over the past few years,” Fitch said in an accompanying statement to the “2016 Outlook: Asia-Pacific Banks.”

“The ratings also reflect concentrated loan books, developing corporate governance standards, and ownership by large family-controlled conglomerates,” it added.

“We believe the Philippine will remain attractive to foreign banks entrants in this environment, and banking sector competition will stay keen overall,” Fitch said.

According to Fitch, a credit rating upgrade for the Philippines will have a corresponding effect on the ratings of DBP, LBP, and potentially, BDO Unibank Inc.

“Such an upgrade may reflect a general improvement in domestic operating conditions and governance standards, which would likely be positive for the overall operating environment and credit profiles of the Philippine banks as well,” it said.

Whilst the state of banks here are healthy, which is good, the key question here is whether the banking industry is really open and competitive such that the economy is well-served. Is there a certain level or cartel-like practices which is holding back the country’s development. Are spreads here fair enough given bank’s cost of funds. If their cost of funds are high, is it because given the good profitability with the status quo, they don’t bother to innovate, and I’m not talking of computerisation, but in reducing their cost of funds. I think this is the basic issue Joe is trying to figure out.

Yep, laying the foundation to dig deeper. The next iteration is to look at some individual banks to see how their balance sheets, income statements, and key ratios compare.

I may not be in a position to comment on this not being a banking expert. What I will say is my own observation. I think the billionaire businessmen here have diversified their investments. Cases in point: The Ayala group who have been into real estate business (Ayala Land Inc and Avida projects nationwide) and we all know that they are into banking – BPI chain which gobbled up Far East Bank, Family Savings Bank and other I can’t remember anymore, so in effect, they have a captured market in housing loans, Same with Henry Sy of SM mall chain whose stall owners are banking at BDO, now in SM Prime Holdings and they have a Banco de Oro who has a captured housing loan market as well. Robinsons, too of the Go family, with Robinson Land Inc. Robinsons Supermarket and Robinsons Bank that takes care of housing loans for their condominium unit buyers. I am not sure about Andrew Tan of Megaworld and San Miguel. Most of these companies have formed the giant Trident group which is responsible for the planned Laguna Lakeshore Expressway Dike (LLED) project.

My two centavo worth comment.

Your observations and contributions are certainly helpful, as indeed from anyone here. This particular comment of yours, I’m sure Joe’s Banking articles will lead us to dig deeper here. How deep is this coupling of real estate business and the banking business, will a crash of one industry pull the other down, are there conflicts of interests, etc. The Glass Stegeaal Act was legislated to separate commercial from investment banking but during the Clinton administration this act was abolished. The integration of these 2 different banking business caused a lot of problem in the last 2 financial crisis in the US. We should be looking at real estate / banking under more or less similar circumstances.

JoeAm, chempo, DAgimas,

Every single time a bank approves a loan, that is adding newly created money into the economy. A growing economy requires this infusion to accommodate and facilitate new or additional economic activity.

If, on the other hand, we accept the notion that you both peddle that what the bank lends are depositors’ money, that banks merely recycle the steady limited supply of money in the system from savers to borrowers, you are painting a picture of what is essentially a stagnant economy, where growth is impossible.

A growing economy requires a growing supply of money.

Now as to whether we should continue allowing private for profit banks to do this infusion is another subject matter that’s open for debate and further discussion.

“That dual ability of banks – the traditional brick and mortar and investment banking – was enabled when the Glass-Steagall Act was abolished and allowed most major banks to engage in excessive risk taking which precipitated the financial crisis of 2008.”

That financial crisis of 2008 resulted in economic problems not only in the US but worldwide. If for every bank loans that these major banks approve, they are adding newly created money into the economy, is that without state regulation? What if the loan availed of in violation of the DOSRI rule through the use of dummies, was not used to produce more goods and services for economic expansion, just hoarded in a secret bank account in Switzerland, in anticipation of a bank’s insolvency and bank run possibility? It follows that a country cannot leave the creation of new money every time a loan is approved and released.

The financial crisis of 2008 should be a lesson learned, don’t you think?

Just an opinion from someone as confused as ever not being an economist nor an expert banker, just someone who wants to understand.

@ Mary

Bank loans do not create new money per se. Pls see my detailed explanation below. It is when the bank loan proceeds are by way of credit to current a/cs, the electronic money, that money is created. Is there a limit to money creation in this way?. If the central bank has reserve requirements, then YES, The max the banking industry can expand money a function of the reserve ratio and the money issued by the govt.. In Phils it is currently 20%, so if Bangko Sentral issues 1,000,000 currency notes and coins (M0) mathematically, the banks can cause money supply to max at 5,000,000.00

Where banking regimes don’t have reserve ratio requirements like UK, then credit expansion is infinity.

Teh Glass-Stegeal Act issue is this — Investment banking is a different kettle of fish. The go deep into financial engineering products, gets excessively levearaged, takes on very high risks (because compensation packages are excessively high), greed comes into play a lot because compensation is tied to profits, their products are often those which are intertwined with various industries such that if one crashes, it creates a knock-down effect across industries and institutions. By allowing commercial banks do all these investment banking stuff a big problem is created. They can allow investment banks to fail, but not commercial bankin because that would affect every segment of the economy.

What is the lesson of 2008 for Philippines banking? Be very careful of financial engineering stuff. Phils is not big into this territory, but I understand there is some real-estate mortgage backed securities which has potential for trouble.

It is not a matter of “peddling” anything, which continues your tendency to belittle views that differ from yours. They differ, not for ill intent, but because they originate from a different operating platform, the business of banking. It sounds like you are back to MMT and proposing that the nation would be well served by manufacturing money at will. The central bank can do that, I suppose, as a matter of policy. Since that is the framework from which you are arguing, I suggest you take that up with them. As for the business of banking, regulatory agencies impose the standards by which banks operate, the level of capitalization being foremost among those standards, and capital gets allocated to different levels of risk. If you want the business of banking to start manufacturing money by pushing out loans without regard for quality, or maybe just giving each depositor 25% interest, then you need to get regulations changed. Banks aren’t the villains. It is the regulators who don’t grasp or buy what you are

peddlingproposing.I don’t think there can be a debate until you consider how regulatory guidelines must change to accomplish what you are arguing for. At some point, you have to get out of the ether of ideology and put specific policies on the table.

SUBJ: BANK LENDING / MONEY CREATION / LOAN FUNDING

Micha, I will make a final attempt to clarify things here by describing in a different way. If you still dis-agree, that’s fine. I’ve taken the trouble to elaborate, so please take the trouble to go through it.

Nobody is refuting the need for money supply to grow in tandem with the economy. I have said few times in past articles on the quantitative relationship of money supply to the GDP.

We are talking 2 different things, but they are related — MONEY CREATION and LOAN FUNDING.

When a bank extends a loan, you have to understand 2 things :

1. It creates a loan asset in their books.

2. There is a matter of the LOAN PROCEEDS. (a) How the borrower wants to take loan – there are many ways; (b)how is the bank going to pay out the loan proceeds.

A. LOAN PROCEEDS BY CASH:

The bank debits Loan a/c and credits Cash a/c.

There is no money creation by the bank.

Bank has given out the loan proceeds to borrower in cash, it’s obligation completed. What the borrower does with the cash (loan proceeds) has no impact on the bank.

B. LOAN PROCEEDS BY CREDIT TO CURRENT A/C :

The bank debits Loan a/c and Credits Borrower’s current a/c.

The bank has created money out of nowhere, by keystrokes. Money supply has increased (because credit a/c balances goes into the M2 statistics).

The bank has transferred the loan proceeds borrower’s current a/c. The bank has satisfied it’s obligation.

When the borrower utilise their loan proceeds (draws on his current a/c) the bank has to fund it.

If borrower draws a cash check, the bank pays out cash.

If borrower draws a payee check, the bank as drawee of the check, need to find FUNDS to pay off the bank that the payee deposits the check into.

Is the original money created by lending bank now extinguished?. No because whilst the lending bank’s current a/c aggregates has gone down, the procceds of the loan utilised by the borrower finds it’s way into the current a/c in another bank. Thus the M2 remains the same.

C. TERM LOAN PROCEEDS BY PAYOUT TO OTHER PARTIES:

Let’s say bank extends a term loan, proceeds in 3 tranches per borrower instruction.

Day of loan approval: Bank opens a Loan a/c — but no balances, because it is not drawn down yet. No money creation, no funding requirement.

Month 1 — Borrower 1st drawing with payment instruction to their current a/c at another Bank (BDO)

Month 2 — Borrower 2nd drawdown with payment instruction to ABC Co Ltd.

Month 3 — Borrower 3rd drawndown with payment instruction to convert to US$ and pay to HSBC (HK) favour XYZ Pte Ltd by SWIFT (telegraphic transfer)

The lender bank has to find funds in months 1,2,3 to pay out as instructed.

The loan proceeds will take the form as instructed by borrower, eg

Month 1 — Banker’s Check in the name of the Borrower who then deposits into their BDO current a/c.

Month 2 — Banker’s Check in payee name ABC Co Ltd, Borrower hand check to payee.

Month 3 — Lender bank converts the loan proceeds from peso into US$, checks who is the US correspondent of HSBC (HK) (let’s say it’s HSBC (NY)), then lender bank makes a SWIFT payment instruction to to their own correspondent bank at NY to pay “HSBC (NY) favour HSBC (HK) for credt ABC Co Ltd.

My illustration of this loan is to show different perspectives.

1. Lender bank has to find the funds at the different loan drawndown dates. — So funding is at time of loan drawings, not loan creation.

2. Is there money creation – there was no current a/c credits to borrower’s a/c at lending bank. So NO credit creation at loan approval stage.

3. Month 1 — money is created when borrower deposits the Banker’s Check into their a/c at BDO. The Loan is in the lender bank’s books, the current a/c in BDO’s books, but M2 has increased because deposit money has increased. So money supply goes up.

4. Month 2 — same as for Month 1. Money is created when ABC Co Ltd deposits the Banker’s Check into their a/c at their bank. Loan is recorded in lending bank, current a/c in another bank. M2 goes up becasue deposit base goes up.

5. Month 3 — Loan is booked in lending bank, but is money created? Is there a current a/c increase in any bank in Phils? NO. So no money creation, no M2 increase.

The points here are:

LOAN CREATION DOES NOT NECESSARILY MEAN MONEY CREATION.

MONEY CREATION OCCURS ONLY WHEN DEPOSIT BASE INCREASE.

INCREASE IN DEPOSIT BASE CAN OCCUR AT LENDER BANK OR SOME OTHER BANKS.

LENDER BANK HAS TO FUND THE LOAN PROCEEDS.

About funding loan proceeds:

When the borrower draws down on the loan the bank must fund it. So where is their funds coming from? Various sources — depositors money, shareholder funds from paid up and undistributed profits of prior years capital, banks borrows from various sources — money markets, debenture bonds etc. The bank’s source of fund is dynamic throughout the day. Every minute of the day it is changing in composition and quantum. Hence in banks there is always a very well paid Treasury Manager, usually one of the highest paid guy there. This guy sits in the most chaotic room in the bank, the dealing room. It’s his job to make sure the bank has funds to meet their credit obligations (plus lots of other stuff). The ALMC sits periodically to monitor and plot their sourcing and funding activities and various other issues like interest rate sensitivities and ageing ladders etc.

Loan proceeds and source of funds are never on a back-to-back basis. The Treasury Manager is the magician. Every day he is like sitting on a pool of funds that is constantly going up and down. At the end of each business day, his pool must be at optimum because this pool is not earning money for the bank, it’s what we call free float. He will end each day with enough in the reserve a/cs and enough minimum balances in their various correspondent bank a/cs all over the world.

About creation:

We have been bantering about fractional banking or bank credit expansion.

For banking regimes with reserve ratio requirements of say 10%, we have talked about how deposits and bank loans expand money supply exponentially. An initial deposit of 1,000 ends up with 10,000 in the money supply. And how you and many new academics scoof at this model. This is just a mathematical model to show how the expansion works overall in the economy.

My illustration above is in conformity with some new academicians ‘revelation’ that loan cycle proceeds the deposit or funding cycle. It is a real world working, we all know that, it’s nothing new.

When it comes to a real world practical situation, things are different. For example, in example C above, if borrower takes the Banker’s Check and deposits into his BDO a/c, does it actually increase money supply? Money supply is theoretically increased only by the initial money printed out by the govt. There is no way anyone can ever ascertain where the lender’s source of funds came from that funded that particular Banker’s check. In other words, each time someone deposits money into current a/c which triggers fractional banking, TRACEABILITY OF SOURCE IS AN IMPOSSIBILITY. And neither is it necessary. The mathematical model for fractional banking simply states that mathematically, with a 10% reserve requirement, the maximum quantum for electronic money to be created is 10 what the govt issued, or the M0.

About inter-bank settlement at Central Bank:

All interbank indebtedness are settled at the central bank. After the Clearing Houses has processed the days transaction, it is all summarised down to a net figure of who owns who how much. The central bank simply passes the relevant entries in their books, YES keystrokes. But that does not mean no money passing hands. The banks must make sure they have funds in their a/cs there. All those new academicians’ revelation of keystrokes, which is correct, but they remain mum on the actual fundings. If it were all just keystrokes, let’s sack all those Treasury Managers in the banks, we don’t need them

@chempo

You are a banker but you are overlooking a very important and fundamental nature of a loan : it is an ASSET of the bank.

Based on your post above, you quibble too much on the liability side of it; or, in your terms, how do banks fund those loans.

It seems to me you are not paying close attention at all to the explanation on how banks satisfy that liability in the video I earlier posted.

Here it is again, and start listening at 6:25 mark ’til at least 9:50 to give you a clear summary explanation for your “funding” concerns.

And yes, as far as “loan funding” is concerned, you can go right ahead and fire that Treasury manager.

Micha Micha

I already told you to discard this video long ago.

I would suggest this Xmas you hold a party with your sister-in-law together with her coleagues from her bank, especially those from Treasury and Operations Dept, and tell them your views of how a bank get its funds by keystrokes.

chempo chempo,

You are not stating which part of the video explanation is wrong.

Video explanation is not wrong, but pepople without deeper operations knowledge will miss out on the point I have been trying to make you understand for so long. And which if you followed by long elaboration above, the question remains where is the funds coming from? Yes interbank settlement is by keystrokes done at central bank, how is one bank going to pay another if they dont have funds in their reserve a/c? In the video eg, last say we start at ‘0’. Both banks have nil balances in their central bank reserve a/c. Now how is central bank going to debit the paying bank who has zero a/c with them? So the paying bank would have to find some funds to put into their reserve a/c.

The video seems simple, but it actually muddles beginners minds. That’s why I say discard that video.

Micha & chempo,

Thanks for this discussion, you guys have had now on 4 threads. I feel like Micha’s showing-off a hot exotic dancer in micro-mini panties all oiled up, and me being not as well versed on this subject want to get lost in all that stuff. And chempo’s the voice reason, telling me, whispering, that’s a guy you’re drooling over.

I don’t know who’s running this whole system, but I hope there’s people like chempo (and Joe), announcing ‘that’s a guy’ (an illusion).

That is a perfect description of what is going on. LOL LOL LOL

If I am not mistaken Joe says that Micha is a he.

RHiro calls Micha a she. As far as I am concerned, until I am corrected,Micha is a….I am confused too.

*******

Ze.

*****

I have no idea if Micha is a he or she, and any gender reference is subconscious and inadvertent.

I’m not saying Micha’s the one all oiled up in a micro-mini panty, guys. I’m saying this MMT, Micha’s pimping is the exotic dancer—- chempo’s the one whispering “that’s a guy” (words of wisdom PFC Pemberton could’ve used).

Like Odysseus and the Lotus eaters, the voice of reason helps a bunch.

Did you say Lotus Eaters?

“Video explanation is not wrong…”

Ladies and gents, chempo the banker says the video is perfectly clear and correct. The universe makes sense. There is hope for mankind. He finally gets it.

Or did he?

“… the question remains where is the funds coming from?”

Incredible. He’s been asking this question a million times and the answer stares at him plainly and clearly in a video explanation he acknowledges as “not wrong”, but for some reason still missed it.

chempo, chempo.

When the bank approved that loan, an account on Robert’s name was simultaneously created. From out of nowhere, there’s now $10,000 on his account. The bank did not harass an ageing pensioner and a lotto winner to deposit their money so they could have that $10,000 lent to Robert. The bank merely typed numbers on Robert’s account and viola, $10,000 is there for Robert to spend anywhere or whichever way he wants.

Now, when Robert proceeds to use that money to buy stuff at, say, Home Depot, how is the bank going to process the payment? Simple. By electronic instruction, Home Depot’s account at bank B is credited and Robert’s account is marked down by corresponding amount. Before the transaction there was $10,000 on Robert’s account. After the transaction there is $0.

Before the transaction, Home Depot’s account at bank B has $50,000. After the transaction, there’s now $60,000.

After that transaction, the total money supply in the broader economy expanded by $10,000; created by the bank and spent into existence by Robert.

Are you following this Mr. Banker?

PS:

Central banks could pump commercial bank reserves through quantitative easing, a process famously described by Ben Bernanke as merely sending electronic instructions to mark up their account balance; a process, further, that is not dependent on generated taxes or income.

Micha

May an accountant but in? In our world, we have not encountered an ex nihilo thing. Only God can create out of nothing. For every action, there is an opposite reaction. In accounting, for every debit, there should be a corresponding credit for our work to be balanced.

In your example, when Robert got his 10,000 loan approved, even if it.s by a keystroke, the bank debits Notes Receivable and credits its account. So they increased an asset (Note Receivable) and decreased another asset (their Cash or current Account. Let’s just say that the 10,000 is part of the bank’s capital, from stockholders’ response to call-in.

Robert, in his personal account gained 10,000 in Cash and records Notes Payable – Bank ABC. Ok, so he goes to Home Depot and gets an item, he issues a check and gets what he purchased. He got his goods, (a debit to capital asset) his checking account got credited, but he still has Notes Payable to Bank ABC.

On the due date, Robert pays the bank, so his Note Payable is cleared, and his cash (let’s say the income derived from the item he got partly from his asset he purchased from Home Depot) was reduced by that amount.

In the Bank ABC’s books, upon receipt of Robert’s payment, they debit their current account and credit the Notes Receivable. The circulating money did not change…but the goods and services did..maybe by the amount of income derived by the bank in interest, and the income earned by Robert, if he invested his loaned money and earned from it, but they did not come from nowhere, it was sourced from the business generated from the loan transaction and from the clients of Robert.

The bank began with zero deposits, but they had capital to begin with, when Robert, their very first client got his loan approved. If another bank has performed that keystroke, then an interbank loan is created, and Bank ABC has a Note Payable to that other bank, instead of decreasing their current cash level.

My simple understanding on how the bank helps the economy wheel to continue turning.

In here, only the regulators get to decide whether to increase money in circulation and they have guidelines to help them decide when and by how much to prevent a run away inflation.

IMHO, our banks are not allowed to create money ex nihilo without ithe The Monetary Authority’s knowledge or approval which is a semi-MMT or practicing monetay sovereignty.